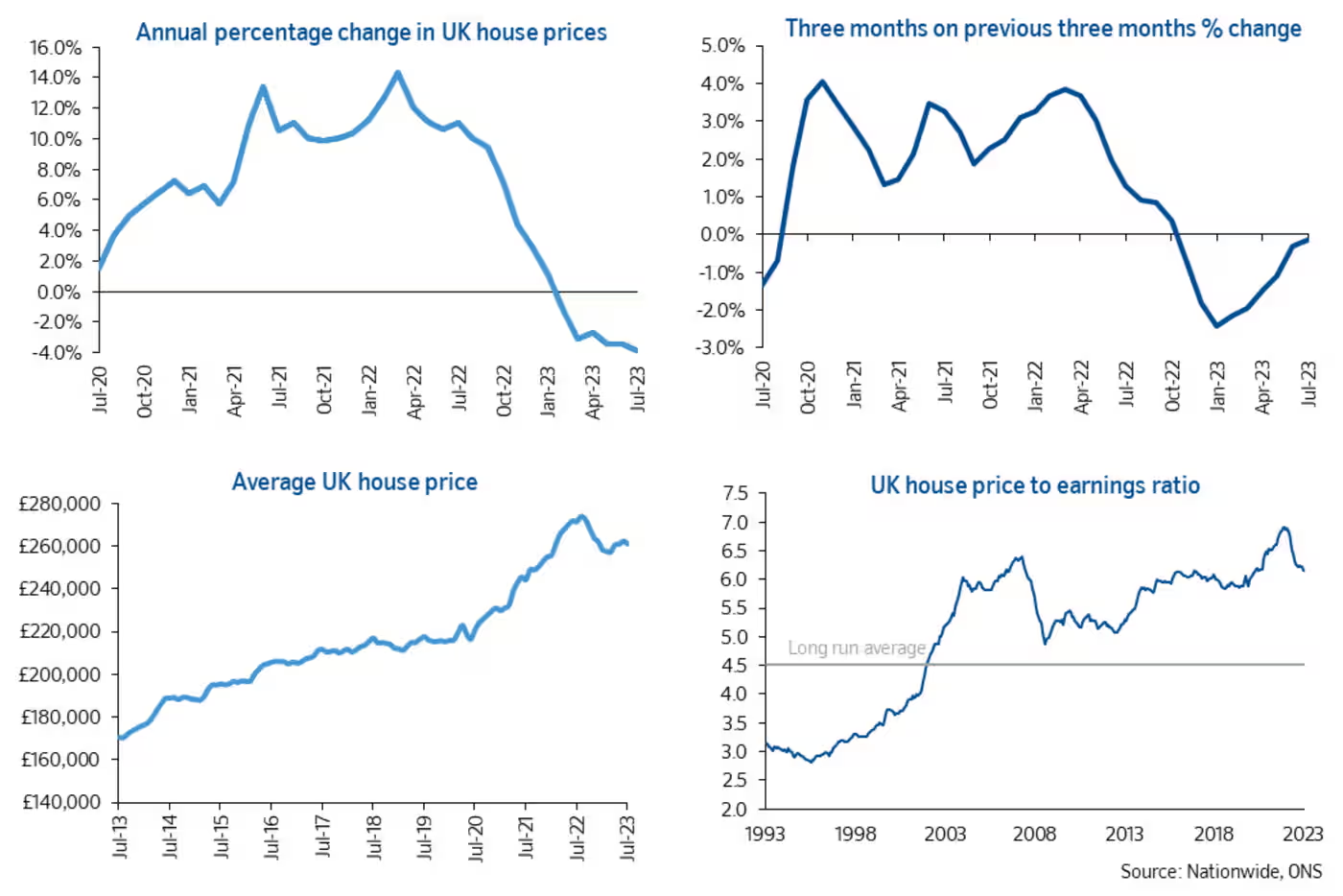

Nationwide reports average house prices fell 3.8% in year to July, biggest annual drop in 14 years, while manufacturers suffer worst month of 2023

House prices: the key charts

These charts from Nationwide show how UK house prices have dropped around 4.5% from their peak last summer, but are still sharply above their pre-pandemic levels.

Knight Frank: Expects prices to fall 5% this year

Estate agent Knight Frank are hopeful that sentiment in the housing market will improve through the rest of this year.

Tom Bill, head of UK residential research at Knight Frank, explains:

“Higher borrowing costs have knocked sentiment and forced buyers to recalculate their budgets but the property market hasn’t slammed on the brakes. The bank rate is nearing its peak, which means that while sentiment will remain subdued, it will only improve in the second half of this year.

That said, prices and sales volumes will come under pressure as the market descends from the highs of the pandemic and adjusts to the new lending environment.

While we expect UK prices to fall by 5% this year, demand should prove more resilient than expected between now and the general election given the cushioning effect of wage growth, high levels of housing equity, lockdown savings, the availability of longer mortgage terms, forbearance from lenders and the popularity of fixed-rate deals in recent years.”

Property lenders also warn that affordability is hitting house prices.

Tomer Aboody, director of MT Finance, explains:

‘The declining number of transactions, combined with negativity in the market, is pushing down property prices, a trend which has been evident for several months.

‘The constant interest rate increases are making affordability difficult for buyers, as they try to make moves, with many waiting until some stability comes in.

‘With some better news on inflation recently, it will be interesting to see whether the Bank of England postpones the next rate rise or goes for a slight increase, giving the market some breathing space to adjust.’

Jeremy Leaf, north London estate agent, says the drop in house prices in July is disappointing – but point out that it only covers buyers taking out a mortgage.

Leaf also confirms that the housing market has softened:

’These figures are a little disappointing considering they are reflecting what was happening in the early to middle part of this year when we saw a rebound in sales before mortgage rates rose significantly.

‘However, Nationwide’s data, though comprehensive and widely respected, can only cover activity of its customers and won’t include the cash buyers who have been dominating the market recently, trying to take advantage of more favourable prices.

‘Clearly, the softening that we have seen in recent months in our offices can take up to a year to show itself in the figures so it may be some while yet before marked differences emerge.’

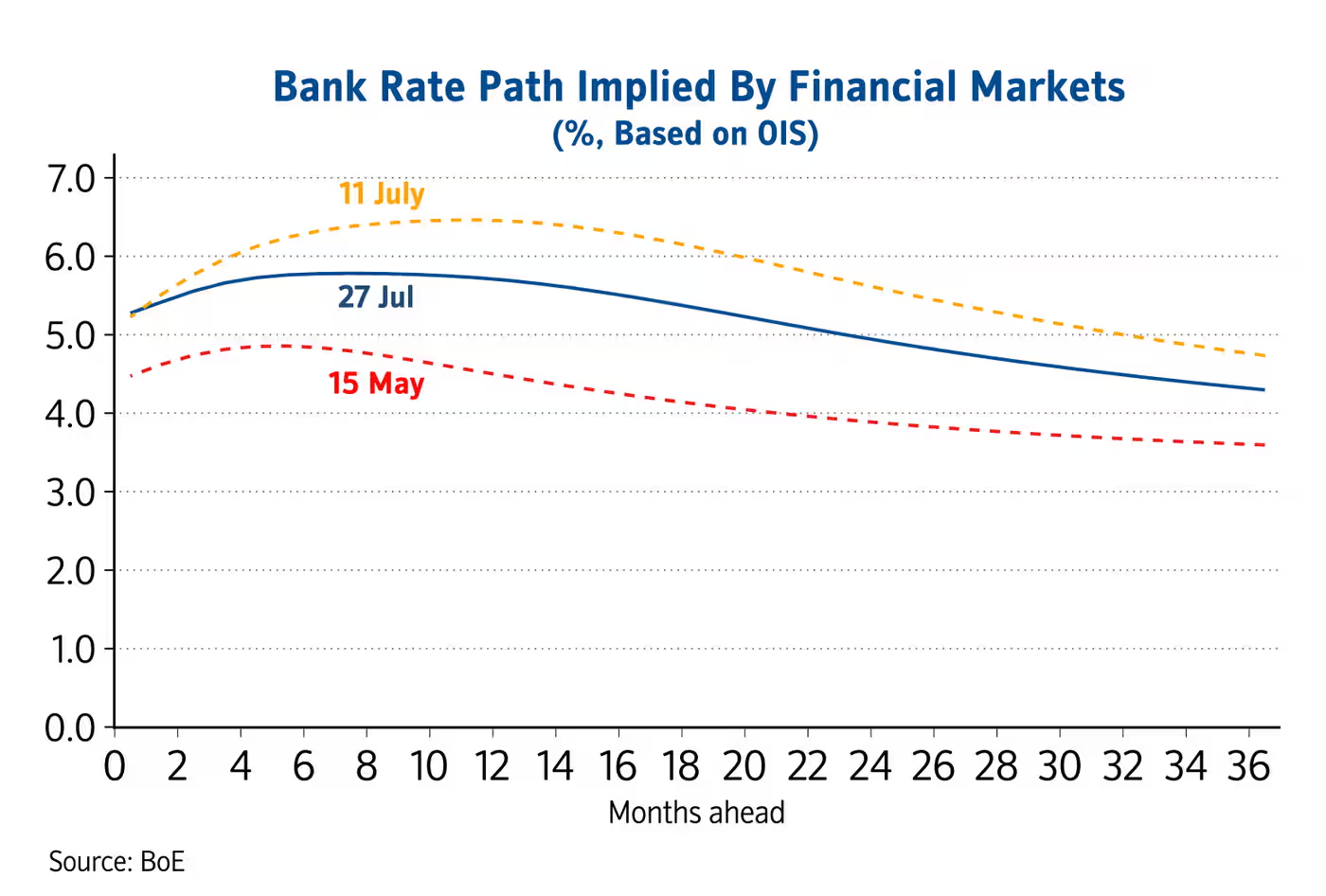

Nationwide also point out that expectations for UK interest rates have been “volatile in recent months”.

In mid-May, the markets expected UK interest rates to peak at 5%. But by early July, that had jumped to 6.5% after UK inflation remained much higher than expected.

Today, though, the peak is expected to be 5.75% next spring, up from 5% today.

Nationwide’s Robert Gardner says:

There has been a slight tempering of expectations in recent weeks but longer-term interest rates, which underpin mortgage pricing, remain elevated.

Nationwide: Affordability should improve once interest rates peak

Nationwide adds that “a relatively soft landing” in the housing market is still achievable, if the economy develops as expected.

Chief economist Robert Gardner explains:

In particular, unemployment is expected to remain low (below 5%), and the vast majority of existing borrowers should be able to weather the impact of higher borrowing costs, given the high proportion on fixed rates, and where affordability testing should ensure that those needing to refinance can afford the higher payments.

While activity is likely to remain subdued in the near term, healthy rates of nominal income growth, together with modestly lower house prices, should help to improve housing affordability over time, especially if mortgage rates moderate once Bank Rate peaks.”

UK house prices fall at fastest rate since July 2009

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

UK house prices have fallen at their fastest rate since July 2009 as rising interest rates cool the property market.

Nationwide has reported this morning that the average house price fell by 3.8% year-on-year in July, the biggest drop since the aftermath of the financial crisis.

That’s an increase on the 3.5% annual drop in house prices in June, and takes the price of a typical home down to 4.5% below the August 2022 peak.

Prices dipped by 0.2% in July alone, on a seasonally adjusted basis, to an average of £260,828, down from £262,239.

Robert Gardner, Nationwide’s chief economist, says the increase in interest rates in recent months have made it more challenging for prospective buyers to afford a mortgage on a new home.

Gardner explains:

For example, a prospective buyer, earning the average wage and looking to buy the typical first-time buyer property with a 20% deposit, would see monthly mortgage payments account for 43% of their take home pay (assuming a 6% mortgage rate). This is up from 32% a year ago and well above the long-run average of 29%.

Moreover, deposit requirements continue to present a high hurdle – with a 10% deposit equivalent to 55% of gross annual average income.

This challenging affordability picture helps to explain why housing market activity has been subdued in recent months. There were 86,000 completed housing transactions in June, 15% below the levels prevailing the same time last year and around 10% below pre-pandemic levels.

More timely mortgage approval data showed a slight increase in activity in June, though most of these applications will pre-date the more recent rise in longer term interest rates. Moreover, activity is still c20% below 2019 levels.

Data from the Bank of England yesterday showed that mortgage approvals in the UK rose to their highest level since October 2022 last month.

That indicates borrowers were scrambling to secure home loan deals earlier this year before interest rates rose higher.